Introduction to the importance of saving for college as a student

Saving for college might seem daunting, but it doesn’t have to be. As a student, understanding how much you need to save can make a world of difference in your financial journey. College is often seen as the stepping stone to future success, yet the costs associated with higher education can feel overwhelming. With tuition rates rising and living expenses piling up, having a solid savings plan is essential.

- Introduction to the importance of saving for college as a student

- Factors to consider when determining how much to save for college

- A. Cost of tuition and fees

- B. Cost of living expenses

- C. Expected financial aid/scholarships

- Tips for budgeting and saving while in school

- Alternative options for funding college:

- A. Student loans

- B. Work-study programs

- The impact of starting to save early

- Case studies

- calclusion

Imagine walking across that graduation stage without the weight of debt hanging over your head or feeling secure knowing you’ve covered all your bases financially. Whether you’re just starting high school or are already enrolled in classes, now is the perfect time to start thinking about how much you should aim to save for college. Let’s dive into what factors come into play when determining that magic number and explore practical tips on budgeting effectively while still enjoying your student years.

Factors to consider when determining how much to save for college

When planning how much to save for college, it’s essential to look at several key factors.

First, consider the cost of tuition and fees. These can vary dramatically depending on whether you’re attending a public or private university. Research your chosen schools thoroughly.

Next, think about living expenses. Do you plan to stay on campus or rent an apartment? Expenses like food, transportation, and utilities should be included in your calculations.

Don’t forget about expected financial aid and scholarships. They can significantly reduce your total costs but aren’t guaranteed. Knowing what you’re likely to receive will help inform your savings goal.

Evaluate any other personal circumstances that could impact costs—like extracurricular activities or specialized programs related to your major—these might add additional expenses worth factoring into your budget.

A. Cost of tuition and fees

When considering how much to save for college, tuition and fees are often the most significant expenses. These costs can vary dramatically depending on the type of institution you choose. Public universities generally offer lower rates for in-state students compared to their out-of-state counterparts.

Private colleges usually carry a higher price tag. It’s essential to research specific schools to understand their tuition structures fully. Some programs may require additional fees that aren’t immediately obvious—lab fees, technology fees, or even special course materials can add up quickly.

Don’t forget about potential increases in tuition over time. Many institutions raise their rates annually, so it’s wise to factor inflation into your savings plan as well. Creating a clear budget will help you assess how much you’ll need each year and guide your saving efforts effectively.

B. Cost of living expenses

When considering how much to save for college, the cost of living expenses is a crucial factor. This involves rent, utilities, groceries, transportation, and personal necessities.

Housing can vary greatly depending on whether you live on-campus or off-campus. On-campus housing might include meal plans but often comes at a premium. Off-campus options can offer savings but may come with added costs like commuting.

Food also takes a sizable chunk out of your budget. Eating in versus dining out affects your finances significantly. Cooking at home usually saves money while allowing for healthier choices.

Transportation costs should not be overlooked either. Whether using public transit or owning a car, consider fuel prices and insurance in your calculations.

Don’t forget about textbooks and supplies that can add up quickly throughout the semester! Planning ahead helps prevent unexpected financial stress during your studies.

C. Expected financial aid/scholarships

When planning how much to save for college, understanding expected financial aid and scholarships is crucial. These resources can significantly reduce your overall expenses.

Begin by researching available scholarships early in your college journey. Many organizations offer awards based on merit, need, or specific talents. Finding the right ones can make a big difference.

Additionally, complete the Free Application for Federal Student Aid (FAFSA) as soon as possible. This form determines your eligibility for federal aid programs and many state-based grants.

Don’t overlook institutional scholarships offered directly by colleges. These can provide substantial funding that’s often overlooked but essential when calculating costs.

Remember that financial aid varies widely between students. Assessing what you might receive helps shape realistic savings goals while keeping stress at bay during college years.

Tips for budgeting and saving while in school

Creating a budget is essential for managing your finances while in school. Start by tracking all your income, including part-time jobs and any allowances. This will help you understand where your money comes from.

Next, list all necessary expenses—tuition, rent, food, and transportation are key players here. Differentiate between needs and wants to prioritize spending accordingly.

Consider using budgeting apps or spreadsheets to keep everything organized. These tools can help visualize expenses versus savings goals.

Save on groceries by meal prepping each week. It’s healthier and usually more affordable than dining out frequently.

Look for student discounts wherever possible; they are often available at restaurants, stores, and entertainment venues.

Set aside a small amount from every paycheck into a dedicated savings account. Even minor contributions add up over time!

Alternative options for funding college:

When it comes to funding college, student loans are often the first thing that comes to mind. They can provide essential financial support, but it’s crucial to understand the terms and repayment plans. Federal loans usually offer lower interest rates and flexible payment options compared to private loans.

Work-study programs present another valuable option. These allow students to work part-time while studying, helping them earn money for tuition or living expenses. It’s a win-win situation where you gain experience and reduce your debt burden at the same time.

Scholarships also deserve mention since they don’t require repayment. Many organizations offer scholarships based on merit or need, so researching these opportunities is key.

Exploring grants can further ease financial pressures. Unlike loans, grants are often awarded based on specific criteria and do not have to be repaid either!

A. Student loans

Student loans can play a crucial role in funding your college education. They help bridge the gap when savings and financial aid fall short.

Understanding the types of student loans is vital. Federal loans typically offer lower interest rates and more flexible repayment options compared to private loans. This can make a significant difference over time.

While borrowing may feel like an easy solution, it’s essential to borrow responsibly. Calculate how much you’ll need for tuition, fees, and living expenses while ensuring you won’t be overwhelmed by debt after graduation.

Researching loan forgiveness programs might also provide relief in certain fields after completing your degree. Some public service jobs even offer benefits that wipe out some of your debt.

Consider all your options carefully before committing to any borrowing decisions. Planning ahead will make managing those payments much easier once you step into the workforce.

B. Work-study programs

Work-study programs offer students a unique opportunity to gain real-world experience while financing their education. These programs can significantly reduce the financial burden of college tuition.

Typically funded by the federal government, work-study jobs may be on-campus or in community service roles. This flexibility allows students to choose positions that align with their skills and interests.

Working part-time while studying helps cultivate essential time management skills, which are invaluable for future careers. Furthermore, these experiences enhance resumes and provide networking opportunities that can lead to post-graduation employment.

It’s crucial for students to explore available work-study options early in their college journey. Many institutions have dedicated resources to help students find suitable placements within various departments or local organizations.

Participating in work-study can ease financial stress and enrich the overall college experience through personal growth and professional development.

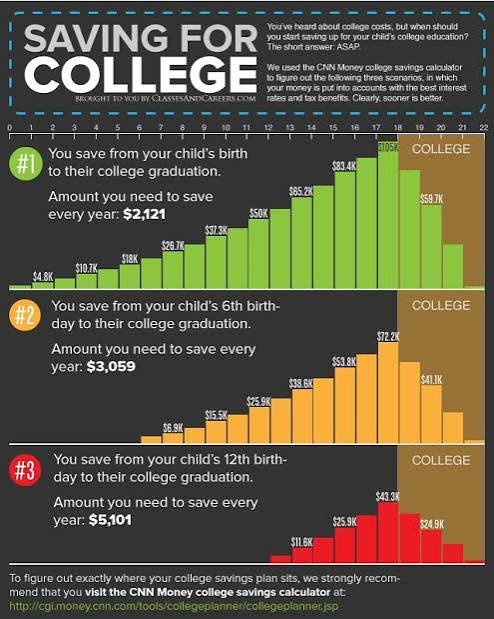

The impact of starting to save early

Starting to save early for college can significantly affect your financial landscape. Time is a powerful ally when it comes to building savings.

When you begin saving during high school or even earlier, the benefits of compound interest come into play. This allows your money to grow over time, making each dollar work harder for you.

Additionally, starting early helps cultivate disciplined saving habits. You learn how to budget and prioritize your expenses well before college begins. These skills will serve you throughout life.

Early savers often feel less stress about finances in their college years. With a solid foundation set in advance, they can focus more on academics and extracurricular activities rather than worrying about tuition costs or living expenses.

Beginning this journey sooner rather than later opens up more opportunities and eases the transition into higher education.

Case studies

Case studies provide real-world insights into the financial journeys of students. For example, Sarah started saving diligently at 16. She worked part-time and set aside a portion of her paycheck each week. By the time she enrolled in college, she had over $5,000 saved.

On the other hand, Mark began saving just before his freshman year. He found it challenging to accumulate funds while juggling classes and a social life. He graduated with student loans that significantly impacted his post-college finances.

These stories highlight different approaches to saving for college. Early savers like Sarah often find themselves less stressed about financial burdens during their studies. Conversely, those who wait may face tougher choices later on.

Examining these experiences can help others make informed decisions about their own savings strategies as they prepare for higher education.

calclusion

Understanding how much to save for college is crucial for students planning their educational journey. The financial landscape can appear daunting, but with careful consideration of various factors, it becomes manageable. Tuition costs and living expenses vary widely depending on the chosen institution and location. Being aware of potential scholarships and expected financial aid also plays a significant role in determining your savings goal.

Budgeting wisely while in school helps create an effective savings plan. Students should explore alternative funding options like student loans or work-study programs to ease the burden of tuition fees and daily expenses.

Starting early gives you a significant advantage when saving for college. It allows compound interest on savings to work in your favor over time, ultimately reducing long-term debt.

Looking at real-life case studies reveals that those who saved consistently from an early age often graduated with less debt compared to peers who started saving later or relied heavily on loans.

Saving for college may seem challenging, but by considering all factors involved and utilizing available resources, students can approach their education without overwhelming financial stress. With proper planning and dedication, achieving your educational goals becomes not just a dream but a reachable reality.